At Heartland, our 10 Principles of Value Investing™ drive our investing process, guiding us toward attractively priced, financially sound, and well-managed businesses with positive earnings dynamics. Our principles, however, are not a collection of discrete variables — they’re intertwined. A good way to see how they’re connected is to focus on companies with strong free cash flow.

There’s an old saying on Wall Street that “cash is king.” At Heartland, we think it’s actually “free cash flow” that reigns supreme. Free cash represents the money a company has left over after paying its bills and making capital expenditures. Businesses that throw off significant free cash have the ability to pay down debt to strengthen their financial health, which is another one our principles. They also have the flexibility to take part in shareholder-friendly strategies, such as repurchasing their own shares, initiating shareholder dividends, raising those payouts, and making accretive, strategic acquisitions. These moves are often catalysts that can get investors to see the true value of a business over time.

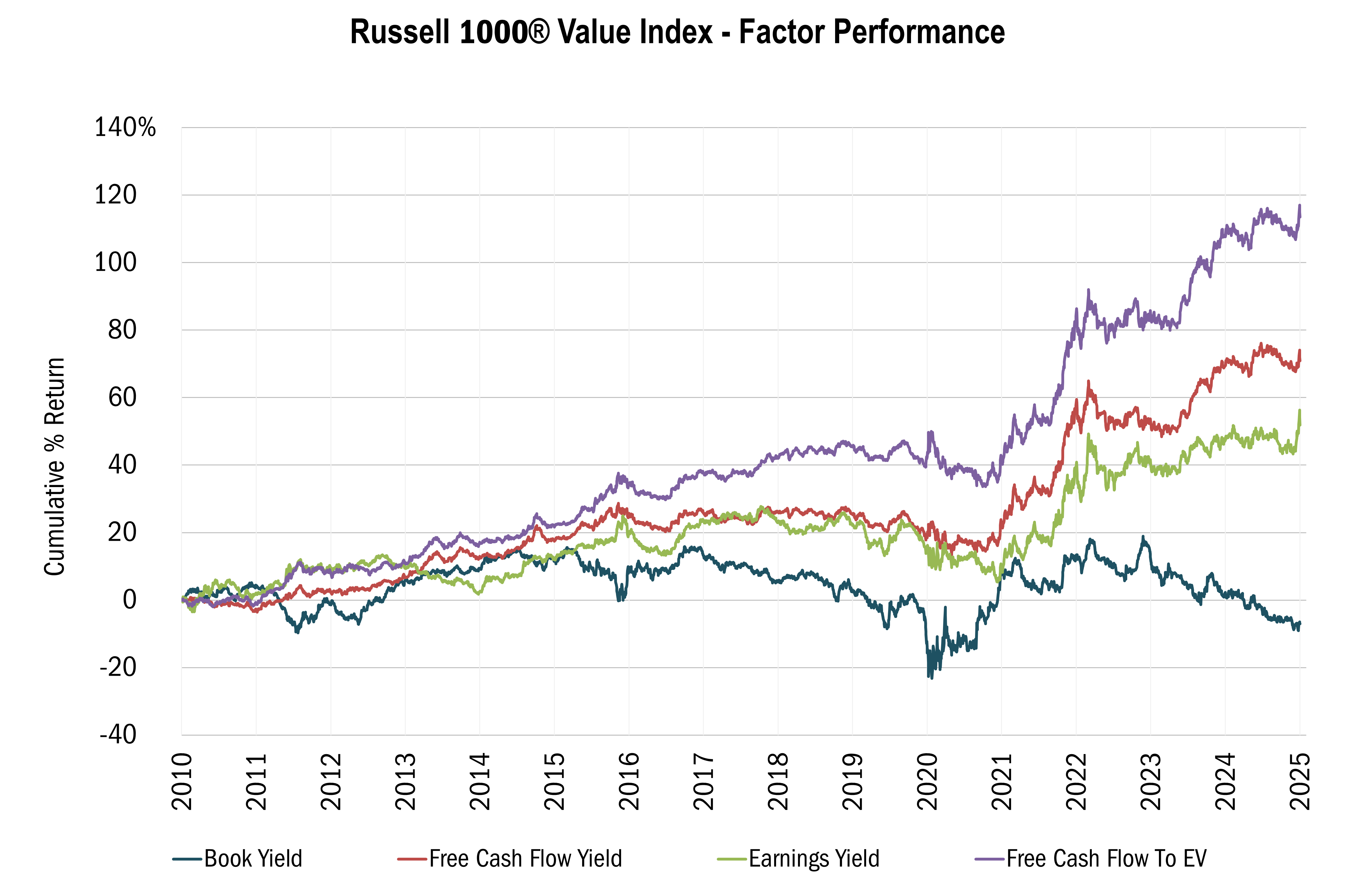

“Catalysts for recognition” is another one of our 10 Principles, as we seek out companies that aren’t just being overlooked but are likely to be recognized soon for what they are truly worth. The good news is, shares of companies that generate lots of cash have historically generated outperformed cash-strapped businesses over the long term (see the chart below).

Source: Piper Sandler & Co. Monthly data 3/12/2010 to 3/12/2025. The data in this chart represents Russell 1000® Index Factor Performance by showing the Cumulative percentage of return over time. Factor Performance is calculated by creating sector-adjusted baskets of stocks in each universe and calculating the relative performance of the top (high) basket against the bottom (low) basket. Quintiling is then used to divide each universe into baskets. The constituents are rebalanced monthly. The sector adjustment process ensures that no basket has a strong sector bias. This is accomplished by first dividing the universe by the GICS sectors. Within each sector, stocks are then ranked by the factor value and are then divided into quintile baskets. Finally, each quintile basket is aggregated across all sectors to assemble the final quintile baskets for the entire universe. This process attempts to create a distribution across sectors in each factor basket that resembles the sector breakdown in the overall universe. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

As this chart shows, companies in the Russell 1000® Value Index with high free cash flow yields (which is determined by taking the inverse of the price/free cash flow ratio) performed better over the past 15 years than other factors such as earnings and book value. However, companies that have thrown off lots of cash relative to their enterprise value performed better still.

Free cash flow/EV is similar to a free cash flow yield calculation, with one big difference: It factors debt — and therefore the balance sheet — into the equation. This is important because a highly levered company generally will not be able use its cash for shareholder-friendly initiatives to the same degree as a business with little or no debt. In this sense, companies with strong cash flow relative to enterprise value are likely to be attractive on not one, but three of our guiding principles: cash flow, financial soundness, and catalysts for recognition.